Reserve Bank of Australia Annual Report – 2015 Banking and Payment Services

The Reserve Bank provides a range of banking, registry and payment settlement services to participants in the Australian financial system, the Australian Government and various international entities. The Bank works closely with its government and agency clients to ensure that they can access services consistent with both their needs and those of the public.

Banking and payment services provided by the Reserve Bank include those associated with the operation of the Australian Government's principal public accounts; transactional banking services to government agencies; custodial and related services; and the operation of the real-time gross settlement (RTGS) system for high-value Australian dollar payments.

Banking

The Reserve Bank's banking services comprise two broad components: core and transactional banking services. Both are provided with the common objective of delivering secure and efficient arrangements to meet the banking and payment needs of the Australian Government and its agencies. In addition, the Bank provides banking and related services to a number of overseas central banks and official institutions.

Core banking services are provided to the Department of Finance on behalf of the Australian Government and the Australian Office of Financial Management (AOFM). These services derive directly from the Reserve Bank's role as Australia's central bank and require the Bank to manage the consolidation of Australian Government agency account balances – irrespective of the financial institution with which each agency banks – into the government's Official Public Accounts (OPA) at the Bank on a daily basis. Balances from agencies' accounts at transactional banks are ‘swept’ to the OPA at the end of each business day, with balances required to meet agencies' day-to-day payment obligations returned the following morning. The average daily sweep to and from the OPA was around $3 billion in 2014/15.

The Reserve Bank also provides the government with a term deposit facility for investment of its excess cash reserves, as well as a short-term overdraft facility to cater for occasions when there is unexpected demand on Commonwealth cash balances. The overdraft facility was used once during 2014/15.

While the Reserve Bank manages the consolidation of the government's accounts, the AOFM has day-to-day responsibility for ensuring there are sufficient cash balances in the OPA to meet the government's day-to-day spending commitments and for investing excess funds in approved investments, including term deposits with the Bank.

The Reserve Bank's transactional banking services are associated with more traditional banking activities. Principal among these are services for making payments from government agencies to recipients' accounts. The Bank processed some 325 million payments, totalling $495 billion, for government agencies in 2014/15. Most of these were made via direct entry. The Australian Government also makes payments by eftpos, the RTGS system and cheque, though its use of cheques has fallen significantly in recent years relative to electronic payment methods. In addition to payments, the Bank provides its government agency customers with access to a number of services through which they can collect funds, including Electronic Funds Transfer, BPAY, eftpos, and card-based services via phone and the internet. The Bank processed 30 million collections-related transactions for the Australian Government in 2014/15, amounting to $460 billion.

The provision of transactional banking services is consistent with the Reserve Bank's responsibilities under the Reserve Bank Act 1959. These services are offered in line with the Australian Government's competitive neutrality guidelines. To deliver the services, the Bank must compete with commercial financial institutions, in many instances bidding for business at tenders conducted by the agencies themselves. It must cost and price the services separately from the Bank's other activities, including its core banking services, and meet a prescribed minimum rate of return. Some 90 government agencies are transactional banking customers of the Bank. Pro forma business accounts for transactional banking are provided in this report, on page 109.

The Reserve Bank works closely with its transactional banking customers and the Australian Government more generally to ensure that they have access to services that are consistent with their needs and those of the public. In 2014/15, the Bank added a second corporate card product to its suite of banking services to provide agency customers with greater choice and convenience in managing expenses. The Bank also broadened the features available through its online payments service, Government EasyPay, allowing its agency customers, in turn, to provide improved services to households and businesses when making payments to government. For some services, the Bank combines its specialist knowledge of the government sector with specific payment services and products from commercial providers to meet the government's banking needs. Many of the services mentioned above, including the new corporate card and the improvements to Government EasyPay, are examples of this. The Bank will continue to make use of combined service arrangements with commercial providers as the government's banking needs evolve.

In common with other financial institutions, the Reserve Bank relies heavily on ICT systems to deliver banking services to its customers and must upgrade and improve its systems over time to ensure that they continue to provide the highest levels of service, reliability and efficiency. Annual reports for the past few years have noted that the Bank is undertaking a program of work to upgrade its banking systems and applications, moving them to a contemporary programming language and architecture, and re-engineering a number of related business processes. Further milestones in this program were reached during 2014/15. In particular, an upgrade to one of the services by which the Bank processes payments made to its agency customers was completed in May 2015. Another significant milestone, involving processing the government's international payments, is scheduled to be reached in the first half of 2015/16.

The Reserve Bank also works with other financial institutions and payments-related organisations to develop and improve banking and payment services at an industry level. Along with other financial institutions, the Bank implemented arrangements during 2014/15 to process cheque payments on the basis of transferring digital images of cheques rather than by the exchange of physical cheques. The move to digital exchanging was an initiative of the Australian Payments Clearing Association and intended to limit increases in cheque processing costs as the use of cheques in the community falls. As noted above, cheque use by the Reserve Bank's government customers has fallen significantly, with cheques now making up less than 2 per cent of agency payments compared with a little under 10 per cent a decade ago.

The Reserve Bank continued its contribution during 2014/15 to developing the payments industry's New Payments Platform (NPP), which will enable payments to be exchanged on a 24/7 basis in near real time together with more complete remittance information. Also, as part of this contribution, work began within the Bank in early 2015 to implement a system to process government-related transactions across the new platform. The Bank expects to make an NPP service available to its agency customers from the payments industry's scheduled go-live date in the second half of 2017. In common with the program to upgrade the Bank's banking systems, the work within the Bank is being overseen by a Steering Committee comprising senior staff. Further information on NPP is available below in the section on Settlement Services.

After-tax earnings from the Reserve Bank's transactional banking services were $5.5 million in 2014/15, around $0.4 million higher than in the previous year. The increase was due largely to increased transaction volumes through the Bank's online collection services. This was tempered slightly by higher costs associated with systems development and service improvements.

Settlement Services

The Reserve Bank owns and operates the Reserve Bank Information and Transfer System (RITS), which provides for the settlement of payment obligations across Exchange Settlement Accounts (ESAs) held with the Reserve Bank. At the end of June 2015, there were 58 institutions approved to operate an ESA, with an additional 30 institutions holding ESAs but having appointed another ESA holder to settle RTGS transactions on their behalf in RITS. A further 86 institutions were Non-Transaction Members of RITS, mostly in order to participate in the Reserve Bank's domestic open market operations.

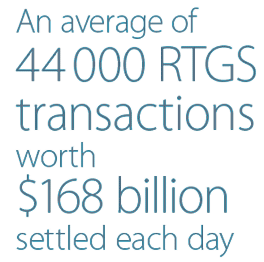

Most transactions are submitted to RITS for settlement individually on a RTGS basis. These include time-critical customer and other bank payments, wholesale debt and money market transactions and the Australian dollar legs of foreign exchange transactions. The latter includes Australian dollar trades settled through continuous linked settlement (CLS), for which net amounts are paid to and received from CLS Bank International each day. Close to 44,000 RTGS transactions, worth $168 billion, were settled in RITS, on average, each day during 2014/15. While RTGS volumes have continued to grow steadily in recent years, growth in values has been more variable, with RTGS values in 2014/15 still well below those of 2010/11.

RITS also settles some payments on a net basis after they have been exchanged. This includes obligations arising from payments exchanged through low-value clearing systems for cheques, debit and credit cards, BPAY and direct entry transactions. Most direct entry obligations are settled on a same-day basis in five multilaterally netted settlements at 10.45 am, 1.45 pm, 4.45 pm, 7.15 pm and 9.15 pm Australian Eastern Time. Obligations arising from cheques, BPAY and retail card transactions, except those for MasterCard, are settled on a multilateral net basis the following day at around 9.00 am. The daily average value of net retail obligations settled in RITS in these six multilateral settlements was $7.4 billion in 2014/15, representing more than $22 billion of underlying transactions.

Other payments are settled on a multilateral net basis using batch feeder functionality in RITS. One of these arrangements is the daily CHESS batch, which effects settlement of payments arising from stock market transactions and is managed by ASX Settlement Pty Limited as Batch Administrator. CHESS batch settlements averaged around $1.1 billion each day in 2014/15.

In late 2014, two new batch arrangements commenced in RITS. On 15 September 2014, MasterCard International became a Batch Administrator in RITS, submitting a daily multilateral net batch for the settlement of obligations arising from domestic MasterCard card use. From 10 November 2014, batch processing has included interbank cash settlements related to some property transactions, as part of a new national electronic conveyancing system for the Australian property industry operated by Property Exchange Australia Limited (PEXA). This initiative is expected to deliver significant benefits to consumers and property industry specialists through efficiency gains and cost savings. The implementation of property settlement in RITS required development work by the Reserve Bank to support the ‘reservation’ of ESA funds in RITS while title changes are lodged with the relevant land titles office. Since commencement, the daily value of property transactions in RITS has increased to around $62 million in June 2015.

The implementation of property settlement batches in RITS is one example of how the Reserve Bank invests in its technical and business infrastructure to ensure that RITS continues to meet the needs of its members and also promotes innovation in the Australian payments system. Another important area where this is occurring is in relation to the industry's NPP project, where the Bank continues to support the industry through its participation in industry design work and project governance and also through the development of the Fast Settlement Service (FSS). The FSS is a new RITS service that will settle individual NPP payments across ESAs in real time, removing the need for financial institutions to manage credit risk and enabling them to complete these customer payments in a matter of seconds.

Reflecting the critical importance of RITS to the Australian financial system, the Reserve Bank requires RITS to be assessed annually against the internationally agreed Principles for Financial Market Infrastructures. These principles, set by the Committee on Payments and Market Infrastructures of the Bank for International Settlements and the Technical Committee of the International Organization of Securities Commissions, aim to ensure the resilience of financial market infrastructures. The 2014 assessment concluded that RITS observed all the relevant principles and supported ongoing work by the Bank to ensure that RITS continues to meet international best practice, including a comprehensive review of its regulations and conditions of operation.[1] Reviews are also being undertaken in the areas of cyber security, operational resilience and participants' compliance with business continuity standards.

The Reserve Bank recovers its operating costs from RITS members through a combination of annual and transaction-based fees. There was a major restructure of RITS fees in July 2012, which sought to provide a more representative distribution of costs among members by striking a better balance in the use of volume and value fees. The process of rebalancing fees continued with an adjustment of fees in July 2014. A further small adjustment to the structure of RITS fees will take effect from July 2015, but this will not materially affect the total value of fees collected.

Around 55 overseas central banks and official institutions hold accounts at the Reserve Bank for settlement of their Australian dollar transactions and over half of these institutions also use the Bank's safe custody services. Overseas demand for Australian dollar investments remains strong, with the face value of securities held in custody by the Bank for these institutions increasing by $3.2 billion to $74.8 billion over 2014/15.

The Reserve Bank also provides settlement services for banknote lodgements and withdrawals by commercial banks and for RTGS settlement of (mainly high-value) transactions undertaken by the Bank and its customers, including the Australian Government.

Footnote

For further details, see Reserve Bank of Australia (2014), 2014 Assessment of the Reserve Bank Information and Transfer System, December. [1]